There is a new site called Footnote, which is dedicated to translating academic work for a general audience. They asked to re-run selected blog posts written by me, and I've agreed. Here is a link to the first one. Presumably more to follow.

So far I like the site. It's clearly still growing, but it's a really good idea and they have a decent cast already assembled. Give it a look.

Tuesday, June 26, 2012

Monday, June 25, 2012

Does Political Science Deserve Public Funds?

If you pay any attention at all to the political science blogosphere you know that the House of Representatives recently decided to prohibit the National Science Foundation from directing $14mn roughly -- 0.2% of its budget -- to political science research. This has caused much consternation among (some) political scientists, as well as indignant blog posts from political scientists and e-mails from APSA asking us to fill in form letters and send them to our Congresspeople.

What it has not done, generally, is come up with any sort of explanation for this event that is informed by political science, nor any sort of strategy for mobilization that would ensure outcomes that benefit the discipline.

This I find ironic. Faced with anbanal existential threat to its existence, political science has responded by a) acting as if social science methods do not exist, and b) acting as if it knows nothing at all about political mobilization, organization, competition, institutions, or much of anything else relevant to altering outcomes in the political sphere. The response from academics has been to whine, get defensive, and generally miss the point (which is almost surely not about whether political science is cool or interesting or even important).

In fact it's worse than simple ineptitude: rather than unifying around some strategy that will secure existing funding, the discipline has turned on itself*.

In a sense I think this goes back to broader schisms in the discipline**. Particularly in IR the past decade-plus has seen a lot of internecine battles over what is best practice for academics. Everything from "what we should study" to "how we should study it" has been debated, quite vituperatively, in journals, blogs, conference panels, graduate student seminars, letters to editors, and bitch-sessions at the tavern. The period from Perestroika to TRIPs has moved us a bit from knee-jerk anti-positivism towards "let a thousand flowers bloom", but there is another problem: the NSF.

Actual funding from the NSF is pretty paltry; getting those funds neither makes nor break political science as a discipline, and almost any NSF-funded project could be funded in other ways***. But getting an NSF grant is prestigious: it improves your application and tenure packets; it can lead to a reduction in teaching load thus increasing research output; it can help you get a full professorship or endowed chair; it boosts your status. Right now the NSF does not fund all types of political science research equally. It privileges certain types of projects, and in particular those smell that smell especially "science-y": studies that build and/or analyze large data sets. As it happens most of my research uses this kind of data set, and I certainly wish there were more of them in the world, but not everybody in political science does. In fact, most of us don't.

According to the most recent TRIPs, a majority of IR scholars consider themselves to be something other than positivists (Q. 26) and only 15% of us employ quantitative methodologies as our primary research method (Q. 28), although another 22% sometimes use them as secondary methods (Q. 29). Obviously international relations is not all of political science, and I'm sure that a greater proportion of Americanists use stats. But (I would expect) fewer comparativists do, and almost no political theorists do. To the extent that NSF funding is biased in favor of quant studies, it is biased against the majority of the discipline. Given that hiring and promotion decisions (and general prestige) are influenced by ability to attract grants from places like the NSF, this is no small thing.

This is probably why Jacqueline Stevens wants to see funding either abolished or distributed via a lottery system which would not privilege some types of work over others ex ante. To me that makes little sense, but I can see why some would prefer either outcome to the status quo ante.

Regardless of where you come down on this -- and I don't really care that much either way -- it's hard not to notice that political science has not covered itself in glory. It seemingly has no theory of politics that can help folks understand why this is happening or how to change it. Its best response to this challenge is classic rent-seeking -- we deserve this money because we do cool stuff -- but without any ability to effectively seek rents. That, in and of itself, might be reason enough to discontinue funding.

*Links to much other discussion can be found at that one. I'm too lazy right now to hyperlink them all myself.

**I'm not the first to point this out. Henry Farrell did as well, in one of the dozens of posts political scientists have dedicated to this bill.

***Phil Arena has one such proposal here, although I'm not too sure how serious he is about it. I find the fact that political scientists are not willing to fund their own research through their professional associations to be another indication that it probably doesn't deserve all that much funding. Some of his commenters suggest that public funding of political science is necessary because it generates public goods which will not be realized without government intervention. To that I say a) show me the evidence****, and b) public goods can be supplied without government intervention, particularly if there are motivated groups who can easily identify the location of those goods and organize to capture them. APSA is already organized, and presumably in a better position to find these public goods than Congress or even the NSF.

****Or even the logic. Most political science research, including NSF-funded research, is published by journals with subscription feeds that are prohibitively for individuals or even most libraries. Therefore the work is most definitely not "non-excludable"... it is excluded! So it is not a public good. But even if it were it would only be a public good in the most facile sense of "the creation and dissemination of knowledge is good" which merely begs the question: maybe, but wouldn't that money be better used in ways that spread knowledge in different ways? E.g., funding public libraries, giving laptops to low-income people, etc.

What it has not done, generally, is come up with any sort of explanation for this event that is informed by political science, nor any sort of strategy for mobilization that would ensure outcomes that benefit the discipline.

This I find ironic. Faced with an

In fact it's worse than simple ineptitude: rather than unifying around some strategy that will secure existing funding, the discipline has turned on itself*.

In a sense I think this goes back to broader schisms in the discipline**. Particularly in IR the past decade-plus has seen a lot of internecine battles over what is best practice for academics. Everything from "what we should study" to "how we should study it" has been debated, quite vituperatively, in journals, blogs, conference panels, graduate student seminars, letters to editors, and bitch-sessions at the tavern. The period from Perestroika to TRIPs has moved us a bit from knee-jerk anti-positivism towards "let a thousand flowers bloom", but there is another problem: the NSF.

Actual funding from the NSF is pretty paltry; getting those funds neither makes nor break political science as a discipline, and almost any NSF-funded project could be funded in other ways***. But getting an NSF grant is prestigious: it improves your application and tenure packets; it can lead to a reduction in teaching load thus increasing research output; it can help you get a full professorship or endowed chair; it boosts your status. Right now the NSF does not fund all types of political science research equally. It privileges certain types of projects, and in particular those smell that smell especially "science-y": studies that build and/or analyze large data sets. As it happens most of my research uses this kind of data set, and I certainly wish there were more of them in the world, but not everybody in political science does. In fact, most of us don't.

According to the most recent TRIPs, a majority of IR scholars consider themselves to be something other than positivists (Q. 26) and only 15% of us employ quantitative methodologies as our primary research method (Q. 28), although another 22% sometimes use them as secondary methods (Q. 29). Obviously international relations is not all of political science, and I'm sure that a greater proportion of Americanists use stats. But (I would expect) fewer comparativists do, and almost no political theorists do. To the extent that NSF funding is biased in favor of quant studies, it is biased against the majority of the discipline. Given that hiring and promotion decisions (and general prestige) are influenced by ability to attract grants from places like the NSF, this is no small thing.

This is probably why Jacqueline Stevens wants to see funding either abolished or distributed via a lottery system which would not privilege some types of work over others ex ante. To me that makes little sense, but I can see why some would prefer either outcome to the status quo ante.

Regardless of where you come down on this -- and I don't really care that much either way -- it's hard not to notice that political science has not covered itself in glory. It seemingly has no theory of politics that can help folks understand why this is happening or how to change it. Its best response to this challenge is classic rent-seeking -- we deserve this money because we do cool stuff -- but without any ability to effectively seek rents. That, in and of itself, might be reason enough to discontinue funding.

*Links to much other discussion can be found at that one. I'm too lazy right now to hyperlink them all myself.

**I'm not the first to point this out. Henry Farrell did as well, in one of the dozens of posts political scientists have dedicated to this bill.

***Phil Arena has one such proposal here, although I'm not too sure how serious he is about it. I find the fact that political scientists are not willing to fund their own research through their professional associations to be another indication that it probably doesn't deserve all that much funding. Some of his commenters suggest that public funding of political science is necessary because it generates public goods which will not be realized without government intervention. To that I say a) show me the evidence****, and b) public goods can be supplied without government intervention, particularly if there are motivated groups who can easily identify the location of those goods and organize to capture them. APSA is already organized, and presumably in a better position to find these public goods than Congress or even the NSF.

****Or even the logic. Most political science research, including NSF-funded research, is published by journals with subscription feeds that are prohibitively for individuals or even most libraries. Therefore the work is most definitely not "non-excludable"... it is excluded! So it is not a public good. But even if it were it would only be a public good in the most facile sense of "the creation and dissemination of knowledge is good" which merely begs the question: maybe, but wouldn't that money be better used in ways that spread knowledge in different ways? E.g., funding public libraries, giving laptops to low-income people, etc.

Wednesday, June 20, 2012

Why Has US Finance Grown? Because The World Is Not a Monad

Guesting at Noah Smith's place, Dan Murphy seeks to explain why the financial sector grew to be such a large component of the US's economy during the 2000s. He offers three possibly explanations: finance became better at "making markets" by matching buyers and sellers, the need to manage risk became more important, and that people became convinced that employing financiars would help them boost their investment portfolios. Murphy suggests that the first two are not good explanations because they are static variables unable to explain change. He doesn't seem to think the third is as well, although it seems that way to me.

I don't think this is the right way to think about this. Instead, I'd rather embed finance into the broader US economy and then embed the broader US economy into the broader global economy. What changes have been taking place in the global economy over the past decade-plus that could help explain this? Two prominent things immediately come to mind:

1. The opening of capital accounts around the world, which began in the 1990s but accelerated dramatically during the 2000s.

2. Changes in the global trading system, particularly the expansion of the GATT -- which added many new members following the end of the Cold War -- and the transition from the GATT to the WTO.

The cumulative effect of these two factors bothforced encouraged the US to pursue its comparative advantage in high-skilled service labor (e.g. finance) and increased the market into which the US could sell its comparative advantage. The result is thus entirely predictable: finance becomes a bigger size of the US's economy, while comparatively disadvantaged sectors shrank. Factor in positive feedback dynamics in global financial markets and this isn't much of a mystery at all.

I don't think this is the right way to think about this. Instead, I'd rather embed finance into the broader US economy and then embed the broader US economy into the broader global economy. What changes have been taking place in the global economy over the past decade-plus that could help explain this? Two prominent things immediately come to mind:

1. The opening of capital accounts around the world, which began in the 1990s but accelerated dramatically during the 2000s.

2. Changes in the global trading system, particularly the expansion of the GATT -- which added many new members following the end of the Cold War -- and the transition from the GATT to the WTO.

The cumulative effect of these two factors both

Tuesday, June 19, 2012

Potential Consequences of the EU's Proposed Regulatory Changes

The European Union is considering a dramatic revision of the current institutional arrangement concerning banking regulation and supervision. Currently, members of the EU must implement international capital standards -- the Basel accords -- but regulation of domestic financial sectors is left up to national governments. Some governments choose to have their central banks regulate, others give that authority to a separate agency; each is fine under current EU rules.

What would the effect of this be? It turns out that I've done some research on that question.* That work suggests that the answer is: it depends. Specifically, it depends on who the regulator would be. The top two choices appear to be the European Central Bank and the European Banking Authority. Why does it matter?

My research, building off of some work by Copelovitch and Singer, argues that giving regulatory authority to central banks alters the policymaking incentives that central bankers face. Without getting too wonky, it incentives central banks to privilege the needs of the banking sector when choosing monetary policy, as financial instability could lead to the loss of their authority. This, in turn, incentivizes banks to behave more riskily, as they expect to receive preferential treatment from sympathetic central banks, so long as they stay above the statutory requirements. The cumulative result is a more bank-friendly monetary regime (the Copelovitch and Singer result) and a more risk-friendly banking sector (my result, supported by a ton of statistical tests). This may not be what the EU currently has in mind.

On the other hand, regulatory central banks may be better able to prevent financial instability in the first place by tailoring policy to the needs of the financial sector. I do not explicitly study this question, and I doubt it is strictly true, but central bankers have argued according to this logic in the past. Alternatively, unifying regulatory and monetary authority could reduce institutional competition and lead to better-coordinated policies. Of course, if that coordination is in a direction that rewards greater risk-taking by EU banks then that might not be the best thing.

*Currently under review so no link, but interested parties can e-mail me for a copy.

That may change. Given the instability in the EU banking markets, and the fact that EU members must allow free movement of capital within the EU, the institution is considering moving supervisory authority to the transnational level:

The leaders of France, Germany, Italy, Spain and Austria are willing to back a powerful supranational supervisor, and a decision to relinquish national control over cross-border banks is being prepared for next week’s EU summit, according to senior officials. One said the new-found political impetus was “astonishing”.The "astonishing" political impetus has come from the fact that the EU is currently experiencing a number of bank runs, capital flight from the periphery to the core, and a general lack of trust in the solvency of many of its financial institutions. To shore up confidence, many in the EU would like to create a "banking union" that would involve continent-wide deposit insurance for EU banks. In exchange for that guarantee, states would have to give up sovereignty to a higher body, which would presumably be heavily influenced by the core European countries (in this case, Britain, Germany, and France).

What would the effect of this be? It turns out that I've done some research on that question.* That work suggests that the answer is: it depends. Specifically, it depends on who the regulator would be. The top two choices appear to be the European Central Bank and the European Banking Authority. Why does it matter?

My research, building off of some work by Copelovitch and Singer, argues that giving regulatory authority to central banks alters the policymaking incentives that central bankers face. Without getting too wonky, it incentives central banks to privilege the needs of the banking sector when choosing monetary policy, as financial instability could lead to the loss of their authority. This, in turn, incentivizes banks to behave more riskily, as they expect to receive preferential treatment from sympathetic central banks, so long as they stay above the statutory requirements. The cumulative result is a more bank-friendly monetary regime (the Copelovitch and Singer result) and a more risk-friendly banking sector (my result, supported by a ton of statistical tests). This may not be what the EU currently has in mind.

On the other hand, regulatory central banks may be better able to prevent financial instability in the first place by tailoring policy to the needs of the financial sector. I do not explicitly study this question, and I doubt it is strictly true, but central bankers have argued according to this logic in the past. Alternatively, unifying regulatory and monetary authority could reduce institutional competition and lead to better-coordinated policies. Of course, if that coordination is in a direction that rewards greater risk-taking by EU banks then that might not be the best thing.

*Currently under review so no link, but interested parties can e-mail me for a copy.

Monday, June 18, 2012

Agreeing and Disagreeing with Kindleberger (and Delong and Eichengreen)

This post is basically to point to the new preface by Brad DeLong and Barry Eichengreen to Kindleberger's The World In Depression 1929-1939. I'm glad the book is being reprinted, and I am in agreement with all of DeLong & Eichengreen's intro. Except this part:

The U.S. and much of Europe was already in depression before the collapse of Creditanstalt. Indeed, chronology suggests that Delong & Eichengreen have causality reversed: the Depression (combined with the fallout from losing WWI, including reparations) caused the collapse of Creditanstalt, not the other way around. U.S. industrial production had fallen by nearly 25% before Creditanstalt's collapse. Farms prices were down by 40%. The financial system was decimated. Trade was collapsing. The signal events occurred in 1929, not 1931. By the latter date we are talking about knock-on effects, not first causes.

My view is not particularly controversial. The collapse of Creditanstalt exacerbated a pre-existing panic, but it did not generate one sui generis.

Contagion is powerful, but it tends to operate from the center outward rather than from the periphery inward.* The best read of the collapse of Creditanstalt is that it was evidence of contagion rather than the epicenter of it.

That said, Kindleberger's book is very good in general, as is the new Delong/Eichengreen intro.

*We've blogged about this before, and we have a piece that will hopefully be forthcoming soon that makes this case explicitly. For a simplistic precis see this Foreign Policy piece that Thomas and I recently placed.

P.S. While thinking about this I stumbled across this piece from a 1952 issue of Time which gets nearly every detail wrong in its first paragraph. For starters: Creditanstalt collapsed in 1931, not 1929; it was not controlled by the Rothschilds until after that collapse; Hitler persecuted the bank during Anschluss for that reason, so it not quite fair to say that the bank "served" Hitler. The rest of the article is blocked to nonsubscribers so I (mercifully) can't read it.

Kindleberger’s second key lesson, closely related, is the power of contagion. At the centre of The World in Depression is the 1931 financial crisis, arguably the event that turned an already serious recession into the most severe downturn and economic catastrophe of the 20th century. The 1931 crisis began, as Kindleberger observes, in a relatively minor European financial centre, Vienna, but when left untreated leapfrogged first to Berlin and then, with even graver consequences, to London and New York. This is the 20th century’s most dramatic reminder of quickly how financial crises can metastasise almost instantaneously.I don't think this is "arguable". First things first... Creditanstalt was decidedly not a "relatively minor" institution; as Ben Bernanke has noted it was one of the largest (and most well-connected) banks in Europe. Moreover, it wasn't the first major bank to fail. To give just one example, the Bank of the United States (a private bank located in New York) failed in December, 1930 -- one of the largest bank failures in U.S. history, which occurred months before the collapse of Creditanstalt. Indeed, in his monetary history of the U.S. Milton Friedman considered the collapse of the Bank of the U.S. as the pivotal moment that tipped the U.S. from recession into depression. In general, financial instability in the U.S. seemed to precede financial instability in Europe from 1929 on.

The U.S. and much of Europe was already in depression before the collapse of Creditanstalt. Indeed, chronology suggests that Delong & Eichengreen have causality reversed: the Depression (combined with the fallout from losing WWI, including reparations) caused the collapse of Creditanstalt, not the other way around. U.S. industrial production had fallen by nearly 25% before Creditanstalt's collapse. Farms prices were down by 40%. The financial system was decimated. Trade was collapsing. The signal events occurred in 1929, not 1931. By the latter date we are talking about knock-on effects, not first causes.

My view is not particularly controversial. The collapse of Creditanstalt exacerbated a pre-existing panic, but it did not generate one sui generis.

Contagion is powerful, but it tends to operate from the center outward rather than from the periphery inward.* The best read of the collapse of Creditanstalt is that it was evidence of contagion rather than the epicenter of it.

That said, Kindleberger's book is very good in general, as is the new Delong/Eichengreen intro.

*We've blogged about this before, and we have a piece that will hopefully be forthcoming soon that makes this case explicitly. For a simplistic precis see this Foreign Policy piece that Thomas and I recently placed.

P.S. While thinking about this I stumbled across this piece from a 1952 issue of Time which gets nearly every detail wrong in its first paragraph. For starters: Creditanstalt collapsed in 1931, not 1929; it was not controlled by the Rothschilds until after that collapse; Hitler persecuted the bank during Anschluss for that reason, so it not quite fair to say that the bank "served" Hitler. The rest of the article is blocked to nonsubscribers so I (mercifully) can't read it.

Friday, June 15, 2012

Room to Move (Redux)

Layna Mosley, one of my professors at UNC, has a piece in Foreign Affairs on the European sovereign debt crisis. In a sense she's come back around to her dissertation work, in which she argued that international investors care much more about outcomes than the particular policies used to generate those outcomes, or things like the partisan composition of governments. Turns out that she was pretty much right about that, at least in the case of Europe.

She has two primary points. The first is that the composition of debt maturity matters quite a lot; a lot of short-term debt means a lot of servicing, which means a greater sensitivity to short-run developments. The second is that investors don't have nearly as much influence on government policies as most commentators ascribe to them. What influence they do have is, again, over outcomes rather than the particular decisions used to reach them. So yes, investors prefer lower debt levels, but they don't particularly care whether fiscal probity is achieved via spending reductions or taxation. Mosley previously referred to this relationship as giving governments "room to move": so long as they stay within certain parameters -- mostly relatively low/stable inflation and relatively low/stable debt levels -- governments have quite a lot of latitude to pursue other policies without being punished by investors.

It's a good piece with valuable lessons. Read it.

She has two primary points. The first is that the composition of debt maturity matters quite a lot; a lot of short-term debt means a lot of servicing, which means a greater sensitivity to short-run developments. The second is that investors don't have nearly as much influence on government policies as most commentators ascribe to them. What influence they do have is, again, over outcomes rather than the particular decisions used to reach them. So yes, investors prefer lower debt levels, but they don't particularly care whether fiscal probity is achieved via spending reductions or taxation. Mosley previously referred to this relationship as giving governments "room to move": so long as they stay within certain parameters -- mostly relatively low/stable inflation and relatively low/stable debt levels -- governments have quite a lot of latitude to pursue other policies without being punished by investors.

It's a good piece with valuable lessons. Read it.

Thursday, June 14, 2012

The Importance of Actors in Networks

(Apologies for the light posting. Real work plus a family emergency has gotten in the way. Normal posting should continue for most of the rest of the summer.)

Ben O'Laughlin recently attended a talk given by Anne-Marie Slaughter to the British Parliament that focused on how the Clinton State Department is trying to lay the groundwork for perpetuating the U.S.-led liberal order. For those who have followed Slaughter's career, both as an academic and as a former senior advisor in Clinton's State Dept, the basics should not surprise. She's a strong advocate of leveraging networks to embed the U.S. at the center of the global system. She believes that one way to do that is via "smart power", a term coined by Joe Nye* and popularized by Sec. Clinton, that emphasizes persuasion as a complement to capabilities. What I found interesting, however, was the way that the State Dept is going about this:

Moreover, once established influencers tend to remain influential. This is because they are already influential. And influencers tend to become influential because of some intrinsic quality. Let's take an example. Bill Gates became influential because of his ability to make personal computing user-friendly and accessible, an intrinsic attribute. But once he gained an initial influence advantage he was able to gain even greater influence simply because he was already influential. This is not an intrinsic attribute of Gates', but rather what is called a "network externality". That is, one advantage of using Gates' products is that many other people are using Gates' products. So Gates attracts new followers largely because he has already attracted followers. In fact, Gates has been able to continue doing this despite the fact that his new products have arguably been inferior, relative to its competitors' products, than his early products. At this point Gates' position as an influencer is almost solely due to his position as an incumbent influencer.

How does this relate to Slaughter's program? It's all fine and good to engage everyone in the world with the U.S.'s message, to encourage everyone to think like stakeholders, and to try to build large coalitions that are broadly supportive of the U.S.'s interests (or at least are not reflexively against them). But this is a very high-cost, low-yield strategy. As O'Laughlin goes on to note, this is a very long-term plan with no guarantee of success. I'd add that if the U.S. cannot simultaneously get the influencers on its side then it is very likely not to succeed in buttressing the liberal order. And if the U.S. can get the influencers on its side then it is very likely to succeed whether it appeals directly to each individual in the world or not.

There's no reason not to do both, but a tactical change from targeting influencers to targeting everyone is misguided, in my view.

What I find interesting about this is contrasting Slaughter's approach with someone like John Ikenberry's. They have both spent their careers theorizing about the liberal order and the U.S.'s hegemonic relationship with it, and have co-authored a bunch of pieces on the subject, but seem now to have diverged in what they think about what needs to be done for it to persist. Ikenberry continues to stress the importance of international institutions, particularly formal institutions. Slaughter has also emphasized formal institutions in the past, particularly legal institutions, but seems not to be shifting focus. There is nothing contradictory about the contemporary work of Ikenberry and Slaughter, but they have diverged a bit in the points they've chosen to emphasize.

*I can use the diminutive because I met him once. That's all it takes, right?

**For one recent study in international relations relating specifically to advocacy networks, see this piece by Charli Carpenter.

Ben O'Laughlin recently attended a talk given by Anne-Marie Slaughter to the British Parliament that focused on how the Clinton State Department is trying to lay the groundwork for perpetuating the U.S.-led liberal order. For those who have followed Slaughter's career, both as an academic and as a former senior advisor in Clinton's State Dept, the basics should not surprise. She's a strong advocate of leveraging networks to embed the U.S. at the center of the global system. She believes that one way to do that is via "smart power", a term coined by Joe Nye* and popularized by Sec. Clinton, that emphasizes persuasion as a complement to capabilities. What I found interesting, however, was the way that the State Dept is going about this:

Slaughter began by saying that structures are being put in place whose effects won’t be visible for some years. The structures the US is building are informed by the assumption that the biggest development in international relations is not the rise of the BRICs but the rise of society – “the people” – both within individual countries and across countries. The US must build structures that harness societies as agents in the international system. Slaughter returned to Putnam’s (1988) two-level game, the proposition that it is in the interaction of international and domestic politics that governments can play constituencies off against one another to find solutions to diplomatic and policy dilemmas. Slaughter took up this framework: the US administration must see a country as comprised of both its government and its society, work with both, and enable US society to engage other countries’ governments and societies. The latter involves the US acting not as “do-er” but as “convenor”, using social media and organising face-to-face platforms for citizens, civil society groups and companies to form intra- and international networks.The bold is added and it's the part that I'm not sure about. A few lines up Slaughter says (via O'Laughlin) that she is "not convinced" on the empirical evidence that influencers are, erm, influential. I wonder why, because it as far as I can tell it's a pretty robust finding across many differential fields that use network analysis.** In network terms, "influencers" generally have a high "degree", meaning that they are at the center of the network and many other actors in the network are linked to them. In many cases, non-central actors are not linked in any way but through the central actor. So if you want to gain influence in the network you get the most bang for the buck by influencing the influencer.

Critically, these two levels are flat. This took me by surprise. At the society level, citizens, civil society groups and companies are connected horizontally. No particular group or individual is afforded a priori centrality. Why is this a surprise? Public diplomacy experts have spent the last few years trying to target ‘influencers’ in societies. Influencers are political, religious or cultural figures who are listened to by others. This idea is informed by network analysis, marketing, and the idea that State Department messages are more credible in different parts of the world when mediated and delivered by a local influential figure than by Hillary Clinton on TV. Slaughter was not convinced by reliance on influencers, empirically or normatively. She argued that all the millions marketers have spent still hasn’t generated any clear knowledge about how influencers can be identified and utilised. Not only that, but it is surely preferable to try to engage whole societies and treat all individuals equally. That would flourish a greater democratic ethos than appealing to amenable clerics, companies, journalists and intellectuals in the hope they might spread the word downwards.

Moreover, once established influencers tend to remain influential. This is because they are already influential. And influencers tend to become influential because of some intrinsic quality. Let's take an example. Bill Gates became influential because of his ability to make personal computing user-friendly and accessible, an intrinsic attribute. But once he gained an initial influence advantage he was able to gain even greater influence simply because he was already influential. This is not an intrinsic attribute of Gates', but rather what is called a "network externality". That is, one advantage of using Gates' products is that many other people are using Gates' products. So Gates attracts new followers largely because he has already attracted followers. In fact, Gates has been able to continue doing this despite the fact that his new products have arguably been inferior, relative to its competitors' products, than his early products. At this point Gates' position as an influencer is almost solely due to his position as an incumbent influencer.

How does this relate to Slaughter's program? It's all fine and good to engage everyone in the world with the U.S.'s message, to encourage everyone to think like stakeholders, and to try to build large coalitions that are broadly supportive of the U.S.'s interests (or at least are not reflexively against them). But this is a very high-cost, low-yield strategy. As O'Laughlin goes on to note, this is a very long-term plan with no guarantee of success. I'd add that if the U.S. cannot simultaneously get the influencers on its side then it is very likely not to succeed in buttressing the liberal order. And if the U.S. can get the influencers on its side then it is very likely to succeed whether it appeals directly to each individual in the world or not.

There's no reason not to do both, but a tactical change from targeting influencers to targeting everyone is misguided, in my view.

What I find interesting about this is contrasting Slaughter's approach with someone like John Ikenberry's. They have both spent their careers theorizing about the liberal order and the U.S.'s hegemonic relationship with it, and have co-authored a bunch of pieces on the subject, but seem now to have diverged in what they think about what needs to be done for it to persist. Ikenberry continues to stress the importance of international institutions, particularly formal institutions. Slaughter has also emphasized formal institutions in the past, particularly legal institutions, but seems not to be shifting focus. There is nothing contradictory about the contemporary work of Ikenberry and Slaughter, but they have diverged a bit in the points they've chosen to emphasize.

*I can use the diminutive because I met him once. That's all it takes, right?

**For one recent study in international relations relating specifically to advocacy networks, see this piece by Charli Carpenter.

Tuesday, June 5, 2012

A Financial Story IPE Folks Should Love

Because it reinforces our priors:

Its membership in the euro currency union hanging in the balance, Greece continues to receive billions of euros in emergency assistance from a so-called troika of lenders overseeing its bailout.

But almost none of the money is going to the Greek government to pay for vital public services. Instead, it is flowing directly back into the troika’s pockets. ...

If that seems to make little sense economically, it has a certain logic in the politics of euro-finance. After all, the money dispensed by the troika — the European Central Bank, the International Monetary Fund and the European Commission — comes from European taxpayers, many of whom are increasingly wary of the political disarray that has afflicted Athens and clouded the future of the euro zone.More here. I have said for awhile now that the story in the eurozone is that the north would keep the south liquid until the north's banks were sufficiently capitalized to handle a default, at which point the money would stop flowing. I thought that would be sometime in 2013 (I think I wrote a post saying that, but can't find it now), but now I think it could be this year.

Why should IPE folks like this story? Because this is the type of tale we tell all the time: "bailout" funds are used to bail out the donor, not the recipient. Just like "aid" funds to the developing world are often tied to certain types of disbursement and are thus a form of subsidy for corporations in the developed world.

There are parallels here (of course) to the Latin American debt crises of the 1980s, where much of the debt was owed to commercial banks in the U.S. The U.S. Treasury pushed for IMF intervention, mostly so U.S. banks could get their money back without the federal government having to officially bail them out. (The story is even more nuanced -- Congress understood what was happening and demanded new regulations of the banking sector, which led to the creation of the first Basel accord -- as Thomas argues here.)

Monday, June 4, 2012

Annals of Silly(?) Policymaking: Procyclical Financial Regulations During a Bank Run Edition

This (via @dandrezer) does not seem smart:

Banks must raise their core tier one capital ratios to 9pc by the end of this month or face the risk of partial nationalisation. The global Basel III rules are also pressuring banks to retrench.

The International Monetary Fund said banks will have to slash their balance sheets by $2 trillion (£1.6 trillion) by the end of next year even in a "best-case scenario".That is only within the European Union, and it came about due to panic over Greece last month. Basically, this means that EU banks have to increase their capital cushions by over 200% by the end of this month. What does that mean?

The Bank for International Settlements (BIS) said cross-border loans fell by $799bn (£520bn) in the fourth quarter of 2011, led by a broad retreat from Italy, Spain and the eurozone periphery.Note that this just in Europe. But it made me wonder (on Twitter): why do this now? After all, it was Germany that insisted on a longer phase-in period for Basel III during negotiations, while the US/UK/Switzerland wanted that stricter capital requirements. Now the EU is doing a rapid phase-in and tougher capital limits years before they are required to by Basel. And they're doing it in the middle of a bank run during a continent-wide recession. What gives? A few things.

1. Banks do have to get to 9% tier 1 capital by the end of the month, but they don't have to come fully into compliance yet. That is, a lot of junk capital that is prohibited by Basel III -- but was allowed under Basels I and II -- will still be allowed. (ht to @Procyclicality for this point)

2. Nevertheless, this is still a big boost to minimum capital standards. So how will banks come into compliance? Two quick and easy ways are to:

a. Hold more cash.

b. Buy more sovereign debt.

The first of these is contractionary -- it's basically hoarding more cash rather than lending it out -- although the ECB can facilitate it if they want to pump eurozone banks full of cash. Non-euro EU central banks, such as the Bank of England, can do the same thing if they want and the US Federal Reserve has injected a bunch of liquidity into foreign banks when needed in the past as well. As a zero-risk instrument, cash has a zero risk weight, so adding more of it to your portfolio brings your overall capital ratio up.

The second of these is expansionary. OECD sovereign debt also carries a zero risk weight under Basel III, as it did under Basels I and II. This might seem bizarre at first, but remember who's making these rules: OECD governments. And OECD governments want to pay low interest on their debt. To do that, they rig the regulatory rules to make it more attractive for financial institutions to buy that debt. Hence, a zero risk weight in Basel.

So what does that mean? If banks need to boost their capital stock, there are two ways to do it: by raising more capital (e.g. by selling equity) or by shifting their risk portfolio. The

Was this the point of this policy? I don't know. Probably it was mostly a freak-out after runs started on Greece and then Spain. But I imagine it was part of the calculus, or at least has become so since. In practice this will likely be a transfer of private funding for public funding. Given that the ECB cannot provide liquidity directly to eurozone governments, but can accept sovereign debt as collateral when lending to banks, this could be part of a stealth bailout program that began when Mario Draghi took over as ECB chief from Jean-Claude Trichet last year. Call it "bailout by regulatory arbitrage".

Will it work? I don't know.

Tuesday, May 29, 2012

Democracy and Development

Xavier Marquez has a very interesting series of posts on the relationship between democracy and economic growth since the end of WWII:

The basics of this relationship in the post-WWII era seem pretty well understood: basically, the richer the country, the more “democratic” it appears to be (in the sense I’ve discussed here and here, where democracy is conceived as a system of normatively regulated competition for control of states including the usual paraphernalia of elections, freedoms of speech and assembly, etc.), though the reasons for why this is the case remain disputed, and there are obvious and significant exceptions to this pattern. Conversely, the academic literature suggests that democratic regimes have a slight and indirect long-term development advantage, though the evidence for this claim is much more controversial, and there is no consensus on how this particular advantage operates, if it exists at allThere are links to literature describing all of these assertions in the original post. Marquez then runs down some simple data (and presents it very well) and notes:

The median income of democratic regimes has been higher than the median income of both hybrid and fully authoritarian regimes since at least the 1950s, and the gap has in general widened, not narrowed, even as the number of democratic countries has increased. (From this graph we cannot tell, however, whether the gap has widened because democratic countries have grown faster, or because non-democratic countries that grew fast turned into democracies; from the graphs below, we may infer that it was a mixture of both). The gap was highest during “peak authoritarianism” in the late 1970s and early 1980s, when most poor and newly independent countries were either hybrid regimes or dictatorships, but it stopped growing after the end of the cold war, when a number of relatively poor countries became democratic. ...

What about growth? Is any particular regime type consistently associated with economic growth? ...The answer is "not really" or at least "not very much". Dictatorships and hybrid regimes have more variability -- some grow very quickly, at least for awhile, but also go bust more frequently -- but averaging across regime types shows very little difference in central tendency:

To the extent that we can ignore these confidence intervals and focus only on the trend performance, democracies have not always done better than these other regimes. In the early post-war era it seems that dictatorships did better (though most did about as well as democracies), but then decolonization came along and the growth performance of dictatorships basically cratered. Indeed, the 80s, when the so-called “third wave” of democratization began, was also (not coincidentally perhaps?) the time when the “growth gap” between democracies and hybrid and dictatorial regimes was at its widest. Ominously, the last decade has seen a reversal of this pattern, which explains much of the (not very well thought out) commentary about the rise of the “Chinese model.”He has a very cool motion chart at his blog (that I can't find the embed code for) that maps out the null effect, so click through to watch it.

Monday, May 28, 2012

More on Cowen on Europe

In his op-ed, Tyler Cowen raises a concern about a euro-collapse that I haven't much seen previously:

1. Does an exit of several peripheral countries from the eurozone constitue an implosion of a reserve currency? I don't think so. The status of the euro as a reserve currency does not depend on Greece's membership, it depends on Germany's management of it. If the alternatives are to jettison Greece -- or even several of the GIPSIs -- or to devalue the currency to keep them in, the euro's status as a reserve currency might actually be improved by a smaller membership of weak countries.

2. How important is the euro as a reserve currency? Roughly as important as the German mark was pre-euro, perhaps in combination with the the franc. The euro has not advanced much above the mark+franc status as a global reserve currency, if any at all, since its introduction in 1999. So the global economy as a whole does not appear to be very dependent on the euro; it is dependent on the US and, to a lesser extent, Germany, Britain, and Japan.

3. Would a euro-exit be more severe than a collapse of a currency peg? It conceivably could, but again: what matters most is Germany, and markets' belief in Germany's credibility to maintain a valuable currency. Germany's economy is not on the verge of collapse, nor does it depend on Greece, and German policymakers have repeatedly chosen to maintain policy credibility over possibly saving peripheral members. How much do markets care about Greece? I'll return to that below.

4. Would a euro-exit signal that one of the world's major economic units doesn't work? No. Greece is not one of the world's major economic units. A euro-exit would signal that one of the world's major political units doesn't work, but I'm not sure that this is new information nor am I sure that markets care all that much. The the extent that markets prefer stability over instability any resolution may be preferable to continued uncertainty.

Let's look at some data. Has the euro has significantly weakened as the crisis has grown more severe?

A bit. But if we zoom out and look at a longer time series we see that the euro is now trading at historical levels:

If Greece leaves will the value of the euro hold? Considering that Greece is by far its weakest link I would think so. Indeed, the fewer non-German members in the euro the more credibility it has! Germany does not need to devalue.

Anyway, just how important is the euro? At the end of last year global dollar holdings were nearly 250% higher than euro holdings. Or consider the exchange market. The introduction of the euro did nothing to reduce the world's reliance on the dollar, as I discuss (and graph) here. The euro is used in roughly the same percentage of the world's Forex as was the mark + franc. The global economy survived the end of those currencies.

There is only one truly important global currency -- the dollar.

Perhaps most distressingly, Cowen seemingly misunderstands the arguments of Kindleberger that he references in the paragraph immediately following the quoted one above:

Think about it this way: if Germany left the euro and re-issued the mark, do you think it would be stronger or weaker than the Germany-less euro? Do you think the new mark would be used more as a reserve currency than the euro or less?

So why should we think that a Greek exit would be much worse than "another depreciation or collapse of a currency peg"?

We thus face the danger that the euro, the world’s No. 2 reserve currency, could implode. Such an event wouldn’t be just another depreciation or collapse of a currency peg; instead, it would mean that one of the world’s major economic units doesn’t work as currently constituted.There are a lot of claims -- some implicit -- in here. I'll take them in turn.

1. Does an exit of several peripheral countries from the eurozone constitue an implosion of a reserve currency? I don't think so. The status of the euro as a reserve currency does not depend on Greece's membership, it depends on Germany's management of it. If the alternatives are to jettison Greece -- or even several of the GIPSIs -- or to devalue the currency to keep them in, the euro's status as a reserve currency might actually be improved by a smaller membership of weak countries.

2. How important is the euro as a reserve currency? Roughly as important as the German mark was pre-euro, perhaps in combination with the the franc. The euro has not advanced much above the mark+franc status as a global reserve currency, if any at all, since its introduction in 1999. So the global economy as a whole does not appear to be very dependent on the euro; it is dependent on the US and, to a lesser extent, Germany, Britain, and Japan.

3. Would a euro-exit be more severe than a collapse of a currency peg? It conceivably could, but again: what matters most is Germany, and markets' belief in Germany's credibility to maintain a valuable currency. Germany's economy is not on the verge of collapse, nor does it depend on Greece, and German policymakers have repeatedly chosen to maintain policy credibility over possibly saving peripheral members. How much do markets care about Greece? I'll return to that below.

4. Would a euro-exit signal that one of the world's major economic units doesn't work? No. Greece is not one of the world's major economic units. A euro-exit would signal that one of the world's major political units doesn't work, but I'm not sure that this is new information nor am I sure that markets care all that much. The the extent that markets prefer stability over instability any resolution may be preferable to continued uncertainty.

Let's look at some data. Has the euro has significantly weakened as the crisis has grown more severe?

A bit. But if we zoom out and look at a longer time series we see that the euro is now trading at historical levels:

If Greece leaves will the value of the euro hold? Considering that Greece is by far its weakest link I would think so. Indeed, the fewer non-German members in the euro the more credibility it has! Germany does not need to devalue.

Anyway, just how important is the euro? At the end of last year global dollar holdings were nearly 250% higher than euro holdings. Or consider the exchange market. The introduction of the euro did nothing to reduce the world's reliance on the dollar, as I discuss (and graph) here. The euro is used in roughly the same percentage of the world's Forex as was the mark + franc. The global economy survived the end of those currencies.

There is only one truly important global currency -- the dollar.

Perhaps most distressingly, Cowen seemingly misunderstands the arguments of Kindleberger that he references in the paragraph immediately following the quoted one above:

We are realizing just how much international economic order depends on the role of a dominant country — sometimes known as a hegemon — that sets clear rules and accepts some responsibility for the consequences. For historical reasons, Germany isn’t up to playing the role formerly held by Britain and, to some extent, still held today by the United States. (But when it comes to the euro zone, the United States is on the sidelines.)I said a bit about that in my post yesterday, and I'll say more about it in another post (this is plenty long already), but if the hegemon is most important than we should really only be concerned about the US (the global hegemon) and Germany (the regional hegemon), not Europe's southern periphery. And the role of the hegemon is to stabilize the system, not necessarily to guarantee good outcomes for every constituent within it.

Think about it this way: if Germany left the euro and re-issued the mark, do you think it would be stronger or weaker than the Germany-less euro? Do you think the new mark would be used more as a reserve currency than the euro or less?

So why should we think that a Greek exit would be much worse than "another depreciation or collapse of a currency peg"?

Sunday, May 27, 2012

The World's Central Banker, Yet Again

Tyler Cowen summons his inner Kindleberger and gets pessimistic:

I'm not going to re-write all those posts here, but please click through and read them. The Fed has been engaged in hegemonic leadership, and has done pretty well so far. Its job is not to put out every fire everywhere; its job is to keep the center of the system intact. So far, at least, its actions have been sufficient.

Note that in the op-ed Cowen more than once sounds a lot like an IPE scholar who has read no IPE literature. That is, he's asking the right questions but fumbles for answers to them. I have other things to write about the piece, but I'm going to break them up into pieces over the next day or two. Consider this a teaser.

We are realizing just how much international economic order depends on the role of a dominant country — sometimes known as a hegemon — that sets clear rules and accepts some responsibility for the consequences. For historical reasons, Germany isn’t up to playing the role formerly held by Britain and, to some extent, still held today by the United States. (But when it comes to the euro zone, the United States is on the sidelines.)It depends on what he means by "on the sidelines". The US Congress is certainly not doing anything about Europe. Short of a Marshall Plan for the GIPSIs I'm not sure what they could do, and there's no way that's happening. But that doesn't mean that the US government as a whole is showing no hegemonic leadership. I've written a number of posts arguing that Bernanke has been acting as the world's central banker during the crisis -- opening swap lines with every major central bank in the world, extending liquidity financing to foreign firms, not provoking currency wars that lead to competitive devaluations, etc. -- and that this has stabilized the core of the global financial system.

I'm not going to re-write all those posts here, but please click through and read them. The Fed has been engaged in hegemonic leadership, and has done pretty well so far. Its job is not to put out every fire everywhere; its job is to keep the center of the system intact. So far, at least, its actions have been sufficient.

Note that in the op-ed Cowen more than once sounds a lot like an IPE scholar who has read no IPE literature. That is, he's asking the right questions but fumbles for answers to them. I have other things to write about the piece, but I'm going to break them up into pieces over the next day or two. Consider this a teaser.

Friday, May 25, 2012

When Did the Dollar Become the World's Reserve Currency?

New research from Livia Chitu, Barry Eichengreen, Arnaud J. Mehl. The abstract:

This paper offers new evidence on the emergence of the dollar as the leading international currency, focusing on its role as currency of denomination in global bond markets. We show that the dollar overtook sterling much earlier than commonly supposed, as early as in 1929. Financial market development appears to have been the main factor helping the dollar to surmount sterling’s head start. The finding that a shift from a unipolar to a multipolar international monetary and financial system has happened before suggests that it can happen again. That the shift occurred earlier than commonly believed suggests that the advantages of incumbency are not all they are cracked up to be. And that financial deepening was a key determinant of the dollar’s emergence points to the challenges facing currencies aspiring to international status.I haven't read it yet, but I'm predisposed to disagree with the conclusion.

Thursday, May 24, 2012

Asymmetry in Global Markets

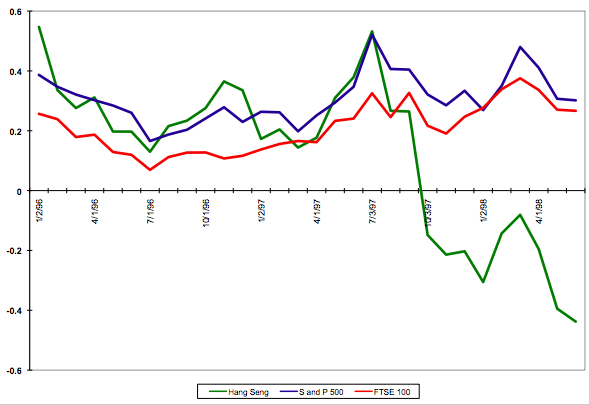

Some argue that we understate the significance of the Asian crisis. So, here are three graphs of equity market correlations in moments of rather severe crisis. The unit in each is 12 month percent change.

1. Black Monday, October 1987. Biggest Single Day Correction in US History. Notice that the FTSE and Hang Seng follow the US down. Notice the correlation 10 years prior to the 1997 Asian crisis.

1. Black Monday, October 1987. Biggest Single Day Correction in US History. Notice that the FTSE and Hang Seng follow the US down. Notice the correlation 10 years prior to the 1997 Asian crisis.

2. The Asian Crisis, 1997. Notice the separation. Hong Kong falls sharply. The US and UK give back a few gains but then recover very quickly. No banks failed in the US as a result of this crisis. And I note that this Asian crisis was probably the most severe to occur prior to 2008. And yet

2. The Asian Crisis, 1997. Notice the separation. Hong Kong falls sharply. The US and UK give back a few gains but then recover very quickly. No banks failed in the US as a result of this crisis. And I note that this Asian crisis was probably the most severe to occur prior to 2008. And yet

3. US Subprime, 2007-09. The rest of the world follows the US down.

So, is Greece more like Thailand, or is Greece more like the United States? We think Greece is more like Thailand.

3. US Subprime, 2007-09. The rest of the world follows the US down.

So, is Greece more like Thailand, or is Greece more like the United States? We think Greece is more like Thailand.

Wednesday, May 23, 2012

Being Relatively Unconcerned About Concerning Things

Blogging has been non-existent the past few days because more pressing work has taken precedence. One such thing was an essay (with Thomas) for ForeignPolicy.com on why we should all be more blase about the Greek situation. It's very counter to the sort of convention wisdom that you can find here (other examples cited in our article).You can read it here. Our central claim:

We may soon see. I hope we don't.

Further economic and financial deterioration in Greece would certainly have negative impacts there and might adversely affect Greece's southern European neighbors, who are facing similar circumstances. But financial weakness in Greece is unlikely to spark a global crisis analogous to the one triggered by Lehman Brothers' collapse in September 2008 -- even if economic woes eventually force Greece to exit the monetary union. Instead, the global consequences of southern Europe's debt crisis are more likely to resemble the Latin American sovereign debt crises of the early 1980s, the East Asian crises of 1997-1998, and Argentina's crisis at the turn of the millennium. Each of these had significant local effects -- widespread bank failures, sharp increases in unemployment, large exchange-rate devaluations, deep recessions -- that were not transmitted globally. Indeed, in each of these cases the global economy continued to grow, major world equity markets held their value, and world trade expanded. None had the dramatic global consequences sparked by Lehman's collapse.We're already getting some pushback -- as we have from the underlying research that informed this piece -- such as this from Dan Drezner:

I think you understated the global impact of the 1997 East Asian crisis. I'd rather avoid another one of those.On the one hand, I agree: I'd rather avoid another one of those, although I don't know how that's possible. On the other, I don't think we understate the global impact of the E. Asia crisis. I think many people dramatically overstate it. The period during which the E. Asian crisis occurred -- the late 1990s -- is associated with one of the largest periods of global economic growth ever. These days we look back on it with nostalgia, and wonder how we can do it again. The E. Asian crisis was a crisis for E. Asia, but not so much for everyone else. I think it's likely that the S. European crisis will be the same. Actually, given the slow-motion nature of the thing, I think it's likely that the S. European crisis will be even less of an event.

We may soon see. I hope we don't.

Monday, May 21, 2012

Brinksmanship and Grexit

Henry Farrell re-ups his view of the eurozone as being a game of brinksmanship between Germany and Greece. I objected to this characterization back in February, and I still don't think it's the best. Take this:

Nor is it necessarily clear (to me) that Germany believes that there is a real chance of catastrophe for them if Greece exits. Perhaps there is, but it's probably not an economic catastrophe. At this point it might be cheaper to shore up the banks than to keep funding Greece indefinitely. Remember that Greece's creditors have already taken very large haircuts. Remember that European banks have had years to prepare for this, and European regulators have (presumably) been forcing them to do so. Euro governments, the ECB, and the EFSF would lose something on the order of €200bn from a full Greek default, of which €75bn would come from Germany. This is not nothing -- about 3% of Germany's GDP -- but it isn't enough to sink Germany either.

More likely Germany is worried about the political ramifications of a break-up of the eurozone, but in that case they should be interested in ensuring that they are not blamed when that happens. This implies that they will engage in negotiations right up until the end, and perhaps even after it, to demonstrate that they made a good faith effort to keep the monetary union intact even if they believe that there is no possible resolution that actually keeps the monetary union intact.

Farrell:

Nor is it clear that a Greek exit would lead to a collapse in Spain, much less Italy, or that such a thing could be avoided even if Greece stays in. The fundamentals are crap either way. It's not clear that a collapse in these countries would be devastating for Germany. They've maintained economic growth thus far, and capital flight from the GIPSIs would likely move into Germany, giving them further fiscal flexibility to deal with their banks and macroeconomy.

Right now the political dynamic in Europe is about who gets the blame for a Greek exit. If blame cannot be assigned in a politically satisfying way then they will continue to muddle through. However the greater the costs associated with keeping Greece in, the more likely the blame will shift away from Germany and the more likely that Germany will refuse to pay on any terms that are acceptable to Greek leaders.

Edward Hugh writes of the choices:

Given that, Germany may wish to re-write it on more stable terms.

There is a very real chance that over a medium term time horizon Germany would be better off with Greece out of the eurozone. If that's the case then this isn't a brinksmanship game.

If there weren’t any possible resolution, there wouldn’t be any incentive to engage in crisis bargaining. What we’re seeing suggests that the players on both sides think that there is a real chance of catastrophe, but also a real chance of a deal.Whether or not there is a possible resolution is most likely private information. (Or, more accurately, neither side knows the truth.) Let's look at this from Germany's perspective. Who are they negotiating with? For all intents and purposes Greece does not have a government that is capable of negotiating. Any future Greek government also has an inability to make a credible commitment to uphold any negotiated settlement in the future, which is why Germany had previously asked for all political parties in Greece -- whether in the government or not -- to approve of the previous bailout program. It is not clear right now who "Greece" is, much less what it is willing to accept.

Nor is it necessarily clear (to me) that Germany believes that there is a real chance of catastrophe for them if Greece exits. Perhaps there is, but it's probably not an economic catastrophe. At this point it might be cheaper to shore up the banks than to keep funding Greece indefinitely. Remember that Greece's creditors have already taken very large haircuts. Remember that European banks have had years to prepare for this, and European regulators have (presumably) been forcing them to do so. Euro governments, the ECB, and the EFSF would lose something on the order of €200bn from a full Greek default, of which €75bn would come from Germany. This is not nothing -- about 3% of Germany's GDP -- but it isn't enough to sink Germany either.

More likely Germany is worried about the political ramifications of a break-up of the eurozone, but in that case they should be interested in ensuring that they are not blamed when that happens. This implies that they will engage in negotiations right up until the end, and perhaps even after it, to demonstrate that they made a good faith effort to keep the monetary union intact even if they believe that there is no possible resolution that actually keeps the monetary union intact.

Farrell:

At a guess, Greece has considerably more bargaining leverage than it might seem to at first. One useful index of bargaining strength is relative levels of sensitivity to breakdown/catastrophe/failure to reach a deal. It’s plausible that Greece is relatively indifferent to breakdown at this point – years of grinding austerity inside EMU seem barely preferable to the costs of exiting the euro. In contrast, Germany could see the collapse of the euro (and consequent very serious economic costs) if a Greek exit leads to the collapse of confidence in Spanish, Irish, and worst of all, Italian banks. If I were to lay a bet on which side is likely to fold first, I’d be putting my money on the Germans.Again, it's not clear who "Greece" is or what their bargaining position is. As Daniel Davies says in comments on Farrell's post, there is no reason to think that Greece is indifferent between staying in or getting out. Something like 80% of Greeks say that they want to stay in. Even Tsipras has stated no intention to exit. The best case scenario of leaving -- probably Argentina -- is not very good, and I wouldn't be optimistic about the best case scenario obtaining in this case. So how much leverage does that really give Greek leadership? If their citizens want to stay in, and the costs of leaving are extreme, then Germany can demand quite a lot.

Nor is it clear that a Greek exit would lead to a collapse in Spain, much less Italy, or that such a thing could be avoided even if Greece stays in. The fundamentals are crap either way. It's not clear that a collapse in these countries would be devastating for Germany. They've maintained economic growth thus far, and capital flight from the GIPSIs would likely move into Germany, giving them further fiscal flexibility to deal with their banks and macroeconomy.

Right now the political dynamic in Europe is about who gets the blame for a Greek exit. If blame cannot be assigned in a politically satisfying way then they will continue to muddle through. However the greater the costs associated with keeping Greece in, the more likely the blame will shift away from Germany and the more likely that Germany will refuse to pay on any terms that are acceptable to Greek leaders.

Edward Hugh writes of the choices:

Right now there are two, and only two, options on the table: help Greece with an orderly exit from the Euro (and crystallise the losses in Berlin, Washington, etc), or print money at the ECB to send a monthly paycheck to all those Greek unemployed. This latter suggestion may seem ridiculous (then go for the former), but so is talk of printing to fuel inflation in Germany (go tell that old wives tale to the marines). If Greece isn’t allowed to devalue, then some device must be found to subsidise Greek labour costs and encourage inbound investment – and remember, given the reputational damage inflicted on the country this is going to be hard, very hard, work.The second of those is not palatable. It would wreck what remains of the political integrity of the Euro project, which has already been corrupted by the less-than-democratic approach to the bailout. Political integrity is not about keeping Greece in on whatever terms... moral hazard is a real risk and the original institutions designed to combat moral hazard (eg Stability and Growth Pact) have been obliterated as has the independence of the ECB. In other words, it's not clear what political integrity Germany would really be fighting for. The entire EU social contract has to be re-written anyway, at least implicitly.

Given that, Germany may wish to re-write it on more stable terms.

There is a very real chance that over a medium term time horizon Germany would be better off with Greece out of the eurozone. If that's the case then this isn't a brinksmanship game.

Sunday, May 20, 2012

Good Sense and Critical Intelligence

Following up on my post below, here's how our elected leaders view social science:

We've been doing the American Community Survey since 1850, and it is used to learn about the demography and needs of the citizenry as a way to guide spending programs in a more sensible way:

Via all the poli sci grad students in my Facebook feed.

“We’re spending $70 per person to fill out [The American Community Survey]. That’s just not cost effective,” [Rep. Daniel Webster] continued, “especially since in the end this is not a scientific survey. It’s a random survey.”I hope you can spot the egregious error at the end.

We've been doing the American Community Survey since 1850, and it is used to learn about the demography and needs of the citizenry as a way to guide spending programs in a more sensible way:

It is the largest (and only) data set of its kind and is used across the federal government in formulas that determine how much funding states and communities get for things like education and public health.The House of Representatives has already voted to abolish it.

Via all the poli sci grad students in my Facebook feed.

Saturday, May 19, 2012

Defending Social Science Against Those Who Would Prefer to Know Nothing

Earlier this week PM included this line in defense of NSF funding for political science at DoM:

Or take this:

In the next paragraph:

Should we accept the validity of bodies of work based only on their perceived "status"? As determined by who, exactly? 40% of Americans don't believe that evolution occurred. Despite clear evidence, only 60% of Americans believe that climate change is happening at all, and a majority believe that humans do not play a major role in altering the climate. Granted, those polls are examples of social science so Gutting would likely give them no credence but even then the question remains: where does this status come from, and why should it matter?

Perhaps more pointedly, everyone should well be concerned about the "validity of the fundamental physics on which our space program was based" considering the impressive number of boondoggles and outright tragedies that resulted from it.

There are many questions of policy relevance that social scientists have not yet answered sufficiently well to base policy on them. There are also many questions with policy relevance that are more or less "settled" by social scientists, in that they have coherent theoretical explanations that are supported by multiple empirical studies. There's no point in running down a list, which could only be illustrative in any case, but one example might be that if you pay people to put silly arguments into print under their own name then they will be more likely to do it than if they were taxed for it.

A bit further down:

Gutting then goes on to suggest that social science's problem is that it cannot do randomized controlled experiments on its subjects and therefore cannot make "detailed and precise predictions". Setting aside the fact that, in many cases, neither can astrophysicists or evolutionary biologists, this is a) changing in the social sciences; b) not a panacea in any science, social or otherwise; c) RCTs are about testing hypotheses (or, sometimes, just seeing what happens) not generating them; d) the analysis of observational data has always been considered a valid way to examine the rightness of theories in the sciences. Should Galileo not have been trusted because he couldn't perform a randomized controlled experiment on the earth's orbit around the sun? Had Darwin no insight on natural selection because he could not perform a trial to determine why the beaks of finches in different places varied in thickness?

Even more absurdly Gutting then writes:

Having painted himself into such a corner Gutting has no choice but to conclude:

More seriously, perhaps we should use research to influence policy decisions when the research is relevant and when there is strong empirical support from multiple research programs, while recognizing that changed circumstances or new information may cause us to modify these programs later. I'm not suggesting that ever will quite happen -- if they notice it all opportunistic leaders will cherrypick findings that support their preferences and disregard the rest -- but surely that's a better goal than relying on the "good sense and critical intelligence" our overlords do not possess to solve our problems.

And when our leaders stray, or when they set policy cynically, it is the role of intellectuals to use every faculty at their disposal to point out the emperor's nakedness. That is easier done with the arsenal of social science at one's disposal than with intuition or impression alone.

Gutting is a professor of philosophy at Notre Dame. It's worrying to see him so dismissive of his colleagues in the academy. Perhaps he should give them some more of his time.

Indeed, the alternative to good social science is not no social science but bad social science.The implication from that is not that all social science is good but that it strives to be, is useful when it is, and in aggregate has improved the stock of human knowledge. Enough has been written about the battle over NSF funding that I feel no need to weigh in, but I must object to this ridiculous post by Gary Gutting at the NYT (via The Monkey Cage). It's titled "How Reliable Are the Social Sciences?" and it argues, I guess, "not enough for it to influence policy". Or in the authors words:

How much authority should we give to such work in our policy decisions? The question is important because media reports often seem to assume that any result presented as “scientific” has a claim to our serious attention. But this is hardly a reasonable view. There is considerable distance between, say, the confidence we should place in astronomers’ calculations of eclipses and a small marketing study suggesting that consumers prefer laundry soap in blue boxes.He then goes on to make a nearly uncountable number of false assertions, misplaced blames, understatements of the usefulness of the social sciences, and overstatements of the development of the natural sciences. It's hard to know where to begin. Take the above quote for starters: The first sentence asks about policy decisions. The concluding sentences reference two potential avenues for inquiry that, so far as I can tell, have nothing whatsoever to do with policy.

Or take this:

But often, as I have pointed out for the case of biomedical research, popular reports often do not make clear the limited value of a journalistically exciting result. Good headlines can make for bad reporting.Biomedical research may have implications for policy -- e.g. what treatments should be covered in insurance plans or something -- but it is not a social science. Additionally, if journalists misread research findings that is an indictment of journalists, not researchers.

In the next paragraph: